It wasn’t that long since the Fed did a surprise pivot towards the end of 2023 backtracking from the hawkish stance they consistently conveyed earlier. That caught many investors by surprise then. And during the FOMC that just happened on 20 March 2024, they doubled down on their pivot. While I wasn’t expecting them to flip, I did not think they would step up their dovishness either.

These are messages that Jerome Powell delivered during the March 2024 FOMC:

1. The US Fed maintained its forecast of 3 cuts this year.

The recent bout of higher inflation readings did not make a dent in their forecast. The dot plot is still showing a slight majority of the Fed members favoring 3-quarter point cuts or more this year. That is not surprising given the only slight uptilt in recent inflation data. I think the markets anticipated this. However, the things and tone that followed were outside of what I thought they would do.

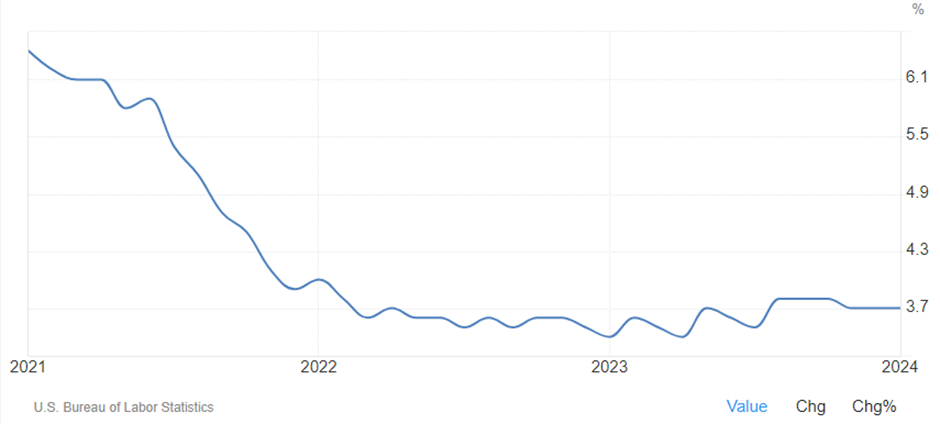

2. A strong labor market alone does not impede cutting rates. A weakening labor market, on the other hand, can also trigger a response.

The US labor market has remained resilient till today. Even though hiring has tapered off significantly from the early post-Covid days and unemployment rose slightly from the lows in 2023, it is well still within the healthy range.

Labor numbers are closely watched by both the market participants and the Fed. Because strong employment and wage growth are key ingredients that fuel inflation. Before the Fed pivoted last year, cooling the labor markets was one of their priority. But this round, Jerome Powell downplayed the impact of the labor market on their rate cut decisions. And as if that is not enough to bring his point across, he added that a weakening labor market, on the other hand, can also lead to a response. While these may look like a simple and logical effort to contrast, it is clearly calibrated to send the markets a dovish signal.

3. Recent inflation data hasn't altered story of inflation coming down to 2% on a sometimes bumpy path.

This is again a fair statement but carefully worded to deliver a dovish undertone. There are many ways he could have chosen to speak on this aside from dismissing higher inflation readings as simply bumps along the way. For example, he could have adopted a more neutral tone and said, “Inflation was higher than expected recently. However, it is not enough to suggest a broader shift in inflation trends. We will need more time to assess.” If he had said this instead, the market reaction could have been entirely different.

4. The Fed will slow its pace of quantitative tightening.

If the previous moves are not enough to show how far the Fed will go in order not to jeopardize the soft landing they are trying to engineer, this one will. Jerome Powell has declared that they will begin to taper its pace of quantitative tightening, or QT, soon. QT only started in 2022 when the Fed allowed up to $95 billion worth of Treasuries and mortgage-backed securities in its holdings to mature every month without pumping its proceeds back into the financial system. Since QT was launched, the Fed’s balance sheet has been reduced by close to $1.5 trillion. Aside from hiking the Fed Funds rate, QT is the other tool that tightens liquidity to slow the economy. By relaxing its pace, this is as good as a declaration that easing has begun.

Why is the Fed suddenly diving the other way?

Some plausible reasons:

1. With inflation data broadly heading lower while the economy is still holding up despite some softening, the Fed sees a good chance of achieving a soft landing. And with more room to maneuver now, they shift their priority towards maintaining growth.

2. The Fed sees potential risks ahead. A notable one is the more than trillion-dollar commercial real estate debt maturing and due for renewal this year and next. This sector has already been battered by tumbling prices and tighter lending conditions. If a significant chunk becomes distressed debts, there will be a fire sale of these properties that will see their prices spiral down further. Banks with exposure to these debts will invariably be implicated and the impact will cascade down to the broader financial markets.

Conclusion

What the Fed does always has heavy consequences down the road both for the broader economy and the financial markets. A key risk is inflation going higher and further eroding the consumption power of the man on the street triggering the need for further hikes. Another is the classic story of fueling asset bubbles. But there is also another school of thought. If the Fed tends to be late, this start of easing which is technically what they are doing now, could also herald the imminent end of this bull market.

Find out ways you can invest through a coffee session!

AllQuant brings to the table a new solution for busy professionals. We put all our 30 years of joint experience across asset management, banking, proprietary trading, and hedge funds to work. And we designed an actively managed multi-strategy model portfolio that is resilient enough to weather different market conditions.

You can now build such a portfolio through iFAST Global Markets without lifting a finger. In this collaboration, we are combining AllQuant’s expertise in hedge fund strategies and iFAST’s advisory capabilities and bringing it to your doorstep.

Ready to start your investment journey? Chat with us over a cup of coffee through a session facilitated by iFAST Senior Investment Adviser, Ou Da Wei, to find out more.

Disclaimer & Disclosure

We are not financial advisers or fund managers. The information published on this Site is provided for informational purposes only. It is not intended to be, nor shall it be construed as, financial advice, an offer, or a solicitation of an offer, to buy or sell an interest in any investment product. Nothing on this site constitutes accounting, regulatory, tax, or other advice.

Any performance shown on this Site is model performance and is not necessarily indicative nor a guarantee of future performance. You should make your own assessment of the relevance, accuracy, and adequacy of the information contained on this Site and consult your independent advisers where necessary.

AllQuant is carrying out introducing activities for iFAST Global Markets (Singapore) as an independent entity and is NOT an agent, servant, employee, representative, or in partnership with iFAST Global Markets (Singapore). AllQuant will be receiving remuneration or introducing fees from iFAST Global Markets (Singapore).

Comments